Are industry estimates for 2026-2027 in the right place? - a framework to contextualize

Not surprisingly, Q3’25 results from the big-3 reported several weeks ago were strong, as were the outlooks for Q4’25.

As often happens after companies beat and raise (especially with Wall Street’s most loved stocks) FY26/27E revenue numbers went up as well.

What we thought was worth highlighting, is the following:

Wall Street often forgets about the “law of big numbers” base effect - y/y % growth is less important than absolute y/y dollar growth

Looking across the big-3, they are expected to deliver $600bn of expected spend in 2026

When online advertising was a smaller % of the total ad budget, you did not need to be as worried about this.

In the US and much of Europe, that number is now likely close to 80% of the advertising pie – it is harder to take share from other channels.

Having been on both the sell-side and buy-side, everybody wants to have a nice and normal y/y deceleration.

The sell-side publishes formal numbers in their earnings recap notes to their investor clientele – “consensus.”

The buy-side has their own views - which will often determine if the stock goes up or down as that number is usually higher or lower than the sell-side.

The easy math is to just have growth slow by 100-150bps per year in each subsequent year from 2026-2028 (We have been guilty of doing this as well, so not going to plead pure innocence).

If Q4’25 ends up being another topline beat quarter vs expectations, you will likely see further upward revisions, potentially exacerbating the issue.

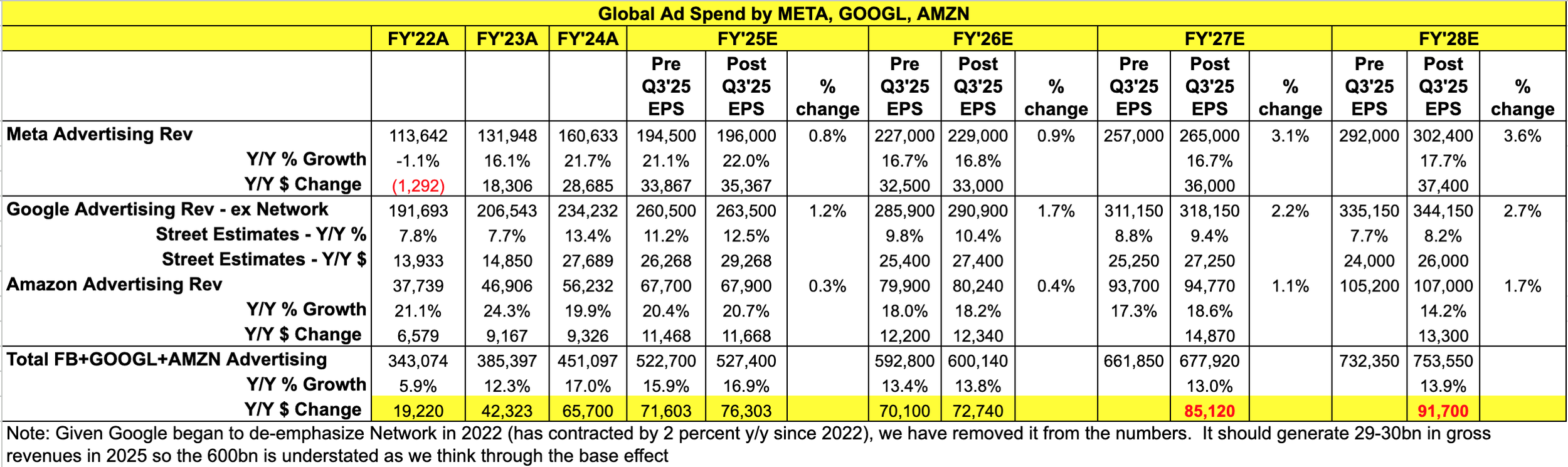

We try to use as few charts as possible so here are the facts:

Let’s look at the numbers

2023 vs. 2022 - 12% y/y and $42bn in y/y dollar growth – A massive rebound year both after a) a weak macro in 2022, b) Meta getting on the other side of its ad-tech stack rebuild post Apple privacy changes.

2024 vs 2023 - 17% y/y and $66bn in y/y dollar growth – Broad-based strength across the space with the biggest shocker vs trend line being Meta – the AI-focused capex investments are clearly making a huge difference

2025E vs 2024 - 17% y/y and $76bn in y/y dollar growth – Almost no deceleration vs 2024 on a % basis, but the pace of dollar growth is not as profound – i.e. the law of big numbers is showing up.

2026E vs 2025E - At $73bn this looks relatively “reasonable” – and there is Y/Y deceleration modeled. Read further about where we think investors need to keep ears open about.

2027E and 2028E - This is where things look aggressive to us – dollar growth Y/Y in 27/26 and 28/27 – at $85bn and $92bn respectively is not so easy.

Ultimately, the market is a discounting mechanism and stocks will be valued on what they are expected to earn in the future. While 2027 is a long way off, by the middle of next year, that is how the street will determine their price targets

Let’s agree on a few Wall Street truisms because they are always true

Sell-side - With consensus numbers now set, the next revision to estimates (generally ex-FX or raises/cuts before previews in January) will be when the companies report their Q4’25 in January/February 2026.

Analysts can write about bear/base/bull cases in their notes, but public estimates are the ones that just got published after Q3’25 EPS.

Buy-side - Stock positioning aside, as well as margin impacts (the bigger negative surprise for Meta off Q3’25 was about investments and capex plans into 2026) – you now believe your Revs/Gross Margins/EBIT/EPS is above or below the street - that drives some investment decisions.

Indisputable facts -

The implications about who “wins” in AI are likely profound, so every Mega-cap company is aggressively investing in the architecture – GPUs, data centers, talent.

Whether or not this capex cycle is justified in 2-3 years, none of the management teams are indicating they intend to moderate spending. We think the losers from this are going to look silly for having poured gasoline on their FCF. That said, these companies view the cost of “losing” as being important enough that they find themselves in a prisoners dilemma.

Win lose or draw, the range of possible outcomes is greater than in almost any time in my investing career. The greater the risks, the more likely that the multiples trade on should be pressured.

Now let’s talk about the puts and takes for 2026

Where there could be more upside

Ongoing AI-driven improvements: These have helped drive performance, and have continued to be tailwinds at the mega-cap ad platforms – Advantage Plus, Performance Max and similar offerings at the smaller platforms. it’s been a couple of years that these have been massive tailwinds- and likely big drivers of outsized growth. Can that continue or does the second derivative catch up to you? Definitely possible.

AI initiatives help drive more SMB onboarding: – the long tail potential at Google and Meta could still be meaningful. Could it become as easy as a) an SMB throws up a website, b) states its marketing objectives, c) those goals and those goals are translated immediately into creative and a tun-key campaign? Put down a credit card and you’re up and running (and spending on ads). The platform has done everything for you.

Meta is in early days of monetizing its other properties – Threads, WhatsApp – the reason Meta has been so successful is they can point the monetization engine at real estate better than anybody.

Agentic commerce/LLM driven behavior changes – Based on Q3’25 earnings from Google, agentic queries and AI Overviews are net-additive to the ecosystem. It is unclear if that will prove out to be true as more behavior shifts away from traditional search, but for now it could be additive.

Where there could be more downside

Micro-economic

TikTok – Doubts about the platform being banned in the U.S are now gone - they will likely be a much greater share taker than previously anticipated from every platform – not just the smaller guys. there are estimates that they will do ~$12bn in US ad revenues.

Estimates range, but best guess is they will do ~$12bn in US ad revenues in 2025. Based on our incremental dollar analysis, if they were to capture an incremental $5-6bn in Y/Y dollar growth it could matter when you look at the incremental dollar math above. They are large enough that somebody is on the margin losing share.

Agentic - Open AI is still in the process of determining how they should come to market with an eCommerce/agentic ad product.

The company has clear ambitions around eCommerce/Search but to compound that, they have introduced Sora – their own video short form app.

If you look further at what was announced at the OpenAI developer conference in early October with the right set of glasses, it is clear that their ambitions extend to the browser and potentially the App Store as you see how they are integrating across different apps in travel and eCommerce.

Challenging Comps – per the chart prior, the Y/Y dollar growth has been strong – irrespective of the winners and losers, the law of big numbers where online ad penetration is now in the high 70% - low 80% (market dependent).

Olympics, World Cup and Elections – Although linear TV is in clear secular decline, the one remaining bastion of TV ratings is live sports. The Olympics and World Cup are always an important TV advertising events, as it often involves both physical sponsorship with TV ad buys. Additionally, the mid-terms elections stand to be a highly important and controversial one, so would expect aggressive spend by both sides of the aisle.

Macro-economic

The Macro economy is clearly getting weaker – there is a reason the fed is finally cutting rates – you are seeing weakness in the labor market. The message out of retailers and restaurants who have reported earnings has been tepid. It’s clear there is stress on the middle- and lower end consumers.

Also worth noting, implosions in the credit market – Zions bank, auto-delinquencies/Carmax implosion are increasing, student loan defaults. These may prove to be idiosyncratic but are yellow flags that justify concerns. At a minimum the lower to mid-income consumer is feeling stress.

Tariff uncertainty - In our discussions with companies earlier this year, in many cases it was less a function of whether the level of tariffs was too onerous – it was a function of clarity. Lack of clarity makes it hard for businesses to forecast their revenues and operating expenses. Tariff “bombs” have largely subsided but the most important one - U.S. China still is an overhang.

We are watching these developments closely, so stay tuned as we will share our views as they emerge.